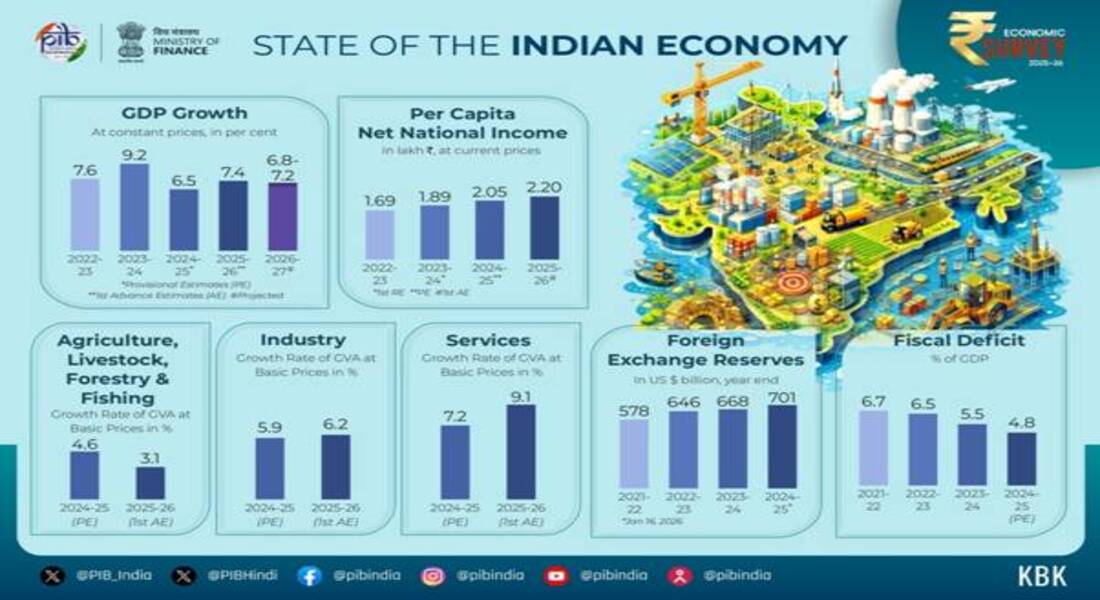

New Delhi: India’s GDP growth for FY26, as outlined in the Economic Survey 2025–26, is estimated at 7.4%, driven by strong domestic consumption and steady investment. The Survey, tabled in Parliament by Finance Minister Nirmala Sitharaman on Thursday, reinforces India’s position as the fastest-growing major economy for the fourth consecutive year.

Looking ahead, the Survey projects real GDP growth of 6.8 to 7.2% in FY27. It also places India’s long-term potential growth close to 7%, reflecting stable macroeconomic fundamentals.

Domestic demand continues to anchor growth in FY26. Private consumption has gained further strength during the year. The First Advance Estimates show that private final consumption expenditure now accounts for 61.5% of GDP. This rise reflects low inflation, stable job conditions, and improving real incomes.

Rural demand has remained firm due to a strong agricultural performance. At the same time, urban consumption has shown a gradual improvement. Tax rationalisation across direct and indirect taxes has supported spending momentum. The Survey notes that consumption growth remains broad-based across regions and income groups, according to an official statement.

Investment has also played a critical role in supporting economic expansion. Gross fixed capital formation stands at 30% of GDP in FY26. During the first half of the year, investment grew by 7.6%. This pace exceeded last year’s growth and stayed above the pre-pandemic average. Public capital expenditure and improved private sector confidence continue to support this trend.

Growth in agriculture and related activities is likely to reach 3.1% during FY26. A favourable monsoon helped farm activity during the first half of the year. Agricultural GVA rose by 3.6% during this period, higher than last year’s growth. However, it stayed below the long-term average.

Allied sectors such as livestock and fisheries maintained steady growth of around 5 to 6%. Their rising share has helped reduce volatility in overall farm output.

The industrial sector has shown visible improvement. Manufacturing expanded by 8.4% in the first half of FY26, beating earlier estimates. Construction activity remained resilient, supported by infrastructure spending and ongoing projects. The sector’s real output share stayed stable, signalling sustained production levels.

High-frequency indicators point to further industrial momentum. Manufacturing PMI, IIP data, and e-way bill generation indicate strong demand. Steel consumption and cement output also recorded steady growth.

The Survey expects industry growth to improve to 6.2% in FY26, helped by GST rationalisation and a positive demand outlook.

On the supply side, services continue to drive growth. Services GVA rose by 9.3% in the first half of FY26. Growth for the full year is estimated at 9.1%. Most service segments have crossed 9% growth. Trade, hospitality, and transport remain slightly below pre-pandemic averages but continue to recover.